Today I explain why most global high yield bonds are really just equity risk, with similar volatility and maximum 40% losses, while also lifting the lid on one of our most complex and bold predictions: the shock Standard & Poor’s upgrade yesterday of the major banks’ hybrids from their previous BB+ “high yield” rating to the all-important BBB- “investment grade” band that will likely fuel large institutional allocations. This is a very complicated forecast that we have been vocal in highligting for a number of years now, which was itself predicated on a range of sophisticated predictions that we had uniquely originated (ie, I don’t know of any other analysts globally who shared this consortium of projections). To read the full column, click here or AFR subs can click here. The final image below is from a presentation I gave this week emphasising that we were calling the hybrid upgrade. Excerpt enclosed:

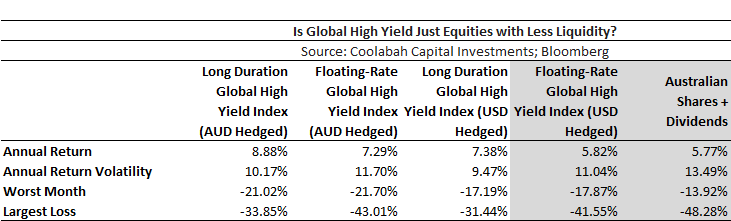

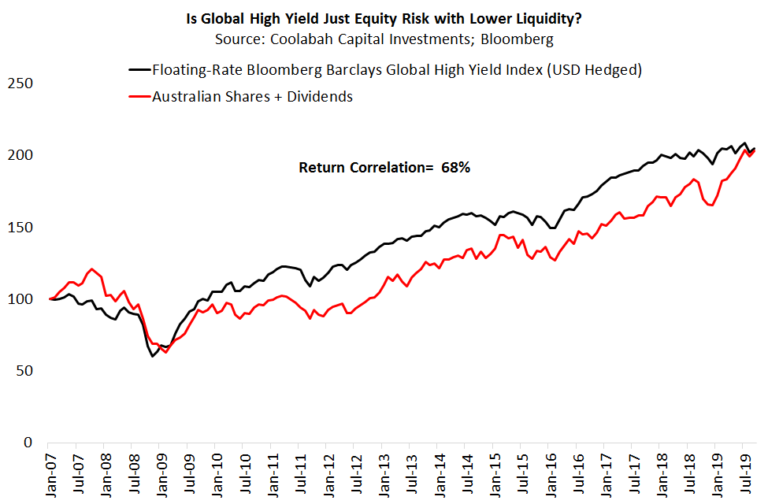

So are some high yield bonds just equities in disguise? We can address this question by comparing the Bloomberg Barclays Global High Yield Total Return Index, which is a flagship measure for the sector, to Aussie shares (plus dividends). My table shows high yield bond returns with fixed-rate duration risk embedded in them, and in “floating-rate” format with the duration hazards hedged out.

Let’s start by focussing on the floating-rate US dollar exposure, because it abstracts away from both the currency hedging and duration impacts. In US dollars, global high yield has delivered exactly the same 5.8 per cent annual return as Aussie shares since January 2007, which captures the impact of the GFC. If you adjusted for franking credits, Aussie shares would outperform on a post-tax basis. The 11 per cent annual return volatility of global high yield is also surprisingly similar to the 13.5 per cent volatility of Aussie shares. If you add-in the historic Aussie dollar currency hedging benefit, high yield outperforms before franking considerations (although hedging is now a 1 per cent annual cost). Throw in interest rate duration risk, and you get another 1.5 per cent annually as long-term yields have fallen.

Volatility is but only one measure of risk. We prefer to look at the worst losses. Global high yield bonds actually have a larger worst monthly loss of 18 per cent relative to Aussie shares’ worst monthly draw-down of 14 per cent. Another risk metric is the peak-to-trough loss. Here again floating-rate global high yield in US dollars is similar to equities with a maximum 42 per cent loss during the GFC versus the 48 per cent loss suffered by listed shares.

This analysis suggests global high yield has a similar risk and return profile to shares. One difference is liquidity. It is easier to buy and sell shares on an exchange than it is to exit over-the-counter sub-investment grade bonds. One alternative is simply to buy high-yielding defensive equities…

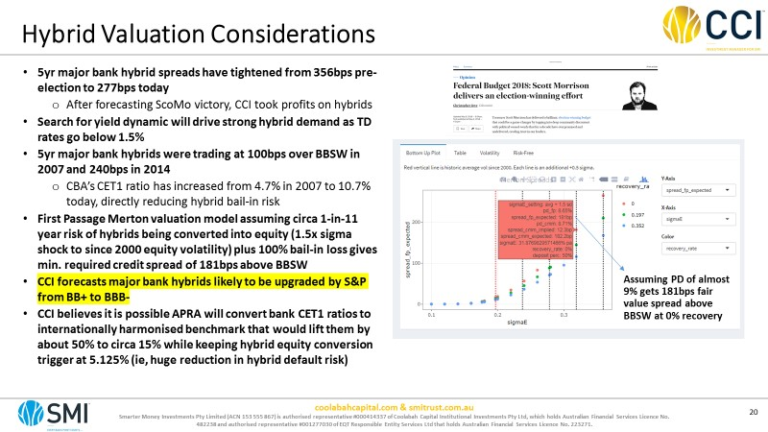

An obvious question is how listed hybrids fit into this mix. Between 2007 and 2019, ASX hybrids have had half the return volatility of the global high yield index. Their worst monthly losses have also been about half that of high yield (peak-to-trough losses were likewise smaller). Performance has been similar, with the ASX hybrid index’s 6.6 per cent annual return over the last five years beating global high yield with and without duration risk. This is despite the fact that major bank hybrids have substantially superior credit ratings to most high yield bonds. Indeed, on Thursday Standard & Poor’s sensationally upgraded major bank hybrids from a “high yield” BB+ credit rating to the all-important “investment grade” band (via a BBB- rating), satisfying one of our boldest predictions.

Since July 2017 I’ve repeatedly forecast that S&P would upgrade the major banks’ hybrid and subordinated bond ratings, which is the outworking of a complex sequence of subsidiary projections. (We don’t know any other analysts who shared this view.)

The logic is as follows. First, in 2017 we predicted that the federal budget would return to surplus years ahead of S&P’s and the market’s expectations, removing a key economic risk. In April 2017 we also forecast that the housing boom would turn into an orderly 10 per cent correction, mitigating Australia’s biggest financial stability hazard. Both these events came to pass. Finally, in April 2019 we were the first to call the sharp recovery in house prices, which is playing out.

The coalescing of these predictions informed our conviction that S&P would upgrade Australia’s “economic risk score”, which it downgraded in May 2017 on housing bubble fears. This has the consequence of reducing the risk-weightings S&P assumes when estimating the major banks’ “risk-adjusted capital” (RAC) ratios, which in turn boosts them above a critical 10 per cent threshold.

APRA’s boss Wayne Byres had previously stated that securing RAC ratios over 10 per cent was a valuable goal for the big banks, because it would lift their stand-alone credit profiles (SACPs) from “a-” to “a”. (When we aired this possibility with the banks many months prior, they laughed at us.)

The higher SACP automatically raises the credit ratings on the major banks’ hybrids and subordinated bonds by one notch (hybrids go to BBB- while sub debt jumps to BBB+). It also reduces the government support assumption underpinning the majors’ AA- senior bond ratings from three notches to two, which is positive for these assets.

Credit for these outcomes can be attributed to prudent fiscal policy, the 2015 resolution of both the government and APRA to force the banks to effectively halve their risk-weighted leverage, and APRA’s efforts since 2014 to thwart housing bubble risks by requiring banks to lend much more carefully.