Today I explain why this housing boom is very different to its predecessors, and should not constrain the RBA from cutting rates further to hit its inflation and employment objectives (click on that link to read or AFR subs can click here). Excerpt enclosed:

House prices are already higher than they have ever been in outright terms – and compared to incomes – before the start of any upswing. Household debt relative to incomes has likewise never been more elevated.

And care of the royal commission and the regulator forcing banks to tighten their lending standards over many years, it has never been more difficult to get a loan from a supervised lender, especially if you are a speculative investor.

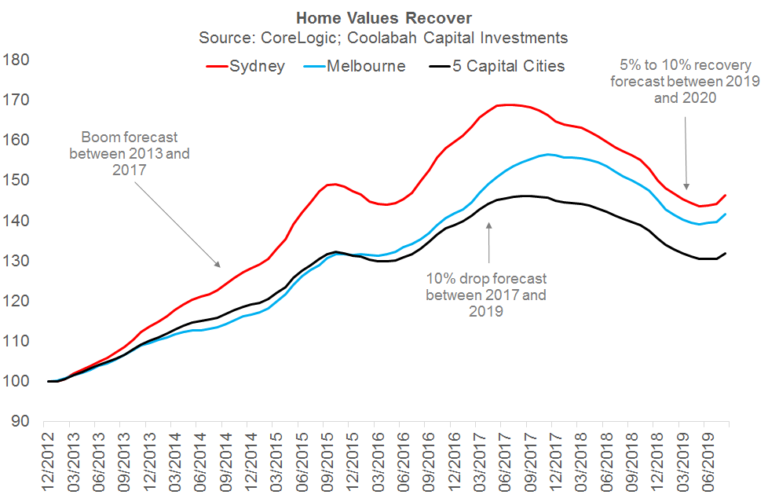

Even if our contrarian April 2019 forecast for a 5 to 10 per cent increase in national house prices over the 12 months following the second RBA rate cut comes to fruition, we will by that time have had no net growth in the value of Australia’s bricks and mortar for more than three years.

That’s because we have benefited from an immensely cathartic 10.7 per cent correction in property prices triggered by APRA’s “macro-prudential” constraints on irresponsible lending, which started in 2014 and progressively ramped up through to early 2017, forcing mortgage rates on investment and interest-only loans markedly higher.

This precipitated the largest drop in home values in modern Australian history, which is frankly exactly what we needed.

In April 2017 when house prices were still appreciating, we projected a 10 per cent decline under the Coalition, which we subsequently warned could rise to 15 per cent under Labor.

Had Scott Morrison not prevailed at the ballot box, it is all but certain Labor’s policies to eliminate negative gearing and hike capital gains tax by 50 per cent would have pushed prices materially lower.

Yet as we look ahead, the RBA now knows that it can safely continue to chisel interest rates lower under the protective veil of APRA’s powerful suite of counter-measures that have a proven history of cauterising financial stability concerns.

This means that a repeat of a speculative, investor-driven bubble fuelled by loose lending is extremely unlikely.